Insurance Drug Testing Requirements 2026: Employer Guide

TL;DR:

- In 2026, federal workplace drug testing regulations focus on SAMHSA’s five-panel screen and updated oral fluid collection procedures. Insurers conduct broader substance tests during underwriting to assess risks and determine premiums. Employers must separately prepare for compliance with federal rules and insurance requirements to avoid legal and financial penalties.

Insurance drug testing requirements in 2026 are defined by two distinct but overlapping frameworks: federal workplace regulations enforced by the Department of Transportation (DOT) and the Substance Abuse and Mental Health Services Administration (SAMHSA), and private insurer underwriting standards that assess substance use to determine coverage eligibility and premium pricing. Employers, HR professionals, and legal advisors must understand both systems because compliance with one does not guarantee compliance with the other. The DOT’s final rule effective june 10, 2026, introduced significant procedural changes, including updated observer terminology and fallback collection procedures, while insurers continue to refine how they interpret drug test results within a broader health profile. Getting both right protects your organization legally and financially.

What are the federal workplace drug testing requirements in 2026?

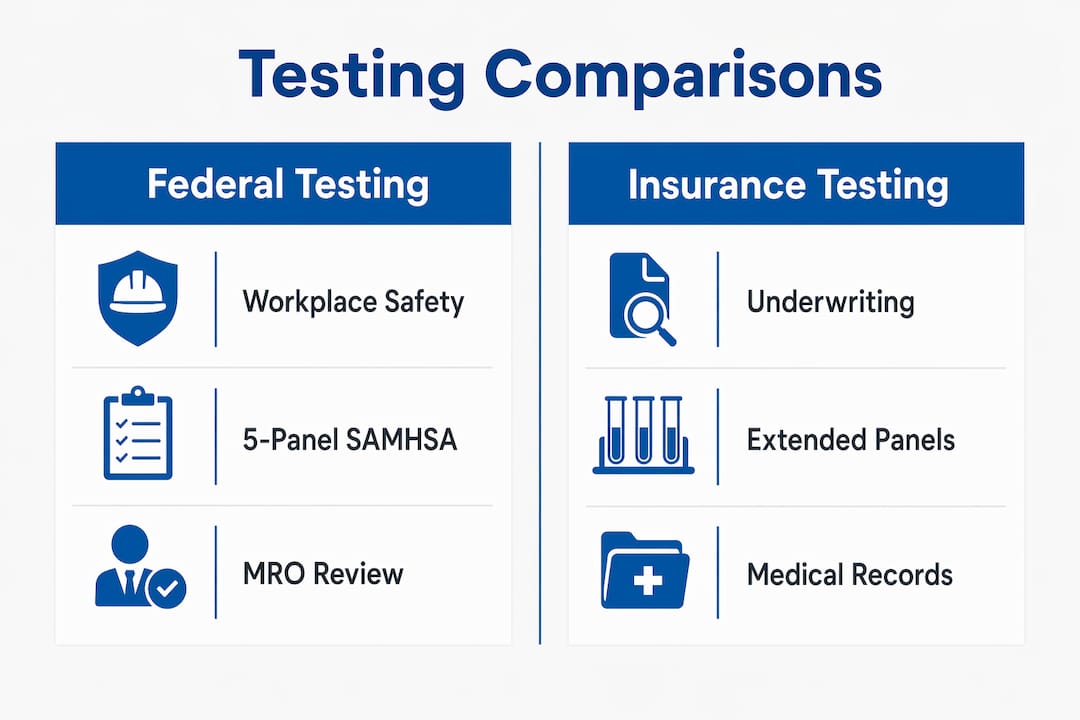

Federal workplace drug testing in 2026 is governed primarily by DOT regulations and SAMHSA-certified laboratory standards. These rules apply to safety-sensitive transportation employees and set the baseline that many non-DOT employers also follow when structuring their own programs.

SAMHSA mandates testing for five substance categories as of may 21, 2026:

- Amphetamines (including methamphetamine and MDMA)

- Cocaine metabolites

- Marijuana (THC metabolites)

- Opiates and opioids (including heroin, oxycodone, and hydrocodone)

- Phencyclidine (PCP)

Specimen validity testing accompanies every collection. These tests confirm the sample is human urine and has not been adulterated or substituted. A specimen that fails validity testing is treated as a refusal to test.

The most significant change in 2026 involves oral fluid testing. The DOT authorized oral fluid collections in 2023, but no HHS-certified oral fluid labs are operational as of mid-2026. That means employers cannot yet use oral fluid as a primary collection method. Until two labs receive certification, employers must conduct directly observed urine collections when oral fluid testing is required under their program. The 18-month transition grace period has not started because the certification threshold has not been met.

The june 10, 2026 rule also updated observer terminology from “gender” to “sex” (male/female) for directly observed collections, aligning with Executive Order 14168. Same biological sex observers are now required for all directly observed urine collections. If a same-sex observer is unavailable at the collection site, the Designated Employer Representative (DER) must be contacted to arrange an alternative site or observer.

Refusing a directly observed collection carries serious consequences. A refusal to test is treated the same as a positive result under DOT rules, triggering disciplinary action and regulatory reporting requirements. Employers must make this consequence explicit in their written policies.

Pro Tip: Review your collection site contracts now. Confirm that each site can provide a same-sex observer on demand and has a documented protocol for contacting the DER when one is unavailable.

How do insurers use drug testing in underwriting in 2026?

Life insurance drug testing is a separate process from federal workplace screening. Insurers collect samples through a paramedical exam, typically at the applicant’s home or a designated clinic, after an application is submitted.

The exam usually includes both blood and urine samples. Urine tests detect substances from a few days up to more than 30 days depending on the substance and frequency of use. THC, for example, can remain detectable in urine for over 30 days in frequent users. Blood tests reflect more recent use, generally within 1–7 days. Insurers use both to build a picture of current and recent substance use.

The substances screened in insurance underwriting often extend beyond the SAMHSA five-panel. Insurers may test for benzodiazepines, barbiturates, nicotine, and alcohol metabolites in addition to the standard categories. The goal is risk assessment, not regulatory compliance, so the panel is driven by actuarial data rather than federal mandate.

Disclosed prescription medications are rarely penalized when the applicant’s medical records confirm consistent, documented use. An applicant taking prescribed opioids for chronic pain who discloses that use upfront is treated very differently from one whose urine shows undisclosed opioid metabolites. Undisclosed or illicit drug use typically leads to application denial, postponement, or significantly higher premiums.

Insurers also consider the timeline of sobriety. Applicants with documented, sustained sobriety and consistent medical management for past substance use have better chances of favorable underwriting outcomes. A two-year clean record with supporting medical documentation carries real weight in underwriting decisions.

For a deeper look at how this process works, the drug testing in insurance underwriting guide from Countrywidetesting covers the full evaluation process in detail.

What are the key differences between federal and insurance drug testing?

Federal workplace testing and insurance underwriting drug testing share some surface similarities but differ in purpose, panel content, and legal implications. Understanding these differences prevents costly compliance errors.

| Feature | Federal (DOT/SAMHSA) | Insurance underwriting |

|---|---|---|

| Purpose | Workplace safety and regulatory compliance | Risk assessment for coverage pricing |

| Specimen type | Urine (oral fluid pending lab certification) | Blood and urine |

| Standard panel | 5 substances (SAMHSA-mandated) | Expanded panel including nicotine, benzodiazepines |

| Detection window | Days to weeks depending on substance | Days to weeks; blood reflects recent use |

| Observer requirement | Same biological sex required for observed collections | No observer; paramedical exam setting |

| Result consequences | Positive = disciplinary action, regulatory reporting | Positive = denial, postponement, or higher premiums |

| Prescription disclosure | Reviewed by Medical Review Officer (MRO) | Evaluated against full medical history |

A clean DOT test does not guarantee insurance eligibility. DOT testing protocols and insurance underwriting processes differ in panel content, cutoff thresholds, and look-back periods. An employee who passes a DOT five-panel urine test may still test positive for substances screened in an insurance exam that fall outside the federal panel.

The Medical Review Officer (MRO) role is specific to federal testing. The MRO reviews all positive, adulterated, substituted, and invalid results before they are reported to the employer. Insurance underwriters do not use an MRO. They evaluate results directly alongside the applicant’s full medical history and disclosed medications.

Pro Tip: Advise applicants to gather all prescription documentation before their paramedical exam. A complete, organized disclosure packet reduces underwriter uncertainty and speeds the review process.

For employers managing both federal compliance and insurance-related screening, the SAMHSA lab certification guide from Countrywidetesting explains how certified labs handle both contexts.

How should employers prepare for 2026 drug testing compliance?

Preparation for 2026 drug testing compliance requires specific, documented actions across policy, procedure, and vendor management. Generic policy updates are not enough.

-

Revise written drug testing policies. Update all references to observer requirements to reflect the june 10, 2026 terminology change from “gender” to “sex.” Confirm that your policy explicitly states that refusal of a directly observed collection equals a positive test result.

-

Update DER standing orders. DER standing orders must specify the exact steps a collection site should take when a same-sex observer is unavailable, including how and when to contact the DER and how to document the situation.

-

Monitor oral fluid lab certification. Employers should monitor the DOT ODAPC website for Federal Register notices announcing HHS-certified oral fluid lab approvals. The 18-month transition grace period begins only after two labs are certified. Missing that notice means missing the window to plan your transition.

-

Audit collection site capabilities. Confirm that every collection site in your network can provide a same-sex observer for directly observed collections. Document their confirmation in writing. Sites that cannot meet this requirement need to be replaced or supplemented.

-

Coordinate with insurance underwriting requirements. If your organization self-insures or manages group health plans, work with your underwriter to align substance disclosure protocols. Employees applying for individual life or disability coverage need clear guidance on prescription disclosure before their paramedical exams.

-

Train HR staff on the distinction between federal and insurance testing. HR professionals who conflate DOT compliance with insurance eligibility create legal exposure. Both processes need separate documentation, separate workflows, and separate communication to employees.

For a complete compliance framework, the drug testing compliance guide from Countrywidetesting covers DOT and federal workplace rules with practical implementation steps.

Key Takeaways

Employers and HR professionals who treat federal drug testing compliance and insurance underwriting drug screening as separate, parallel obligations will avoid the most common and costly compliance failures in 2026.

| Point | Details |

|---|---|

| Federal testing is DOT/SAMHSA-driven | The five-panel SAMHSA standard applies to safety-sensitive roles; oral fluid testing remains on hold pending lab certification. |

| Observer rules changed june 10, 2026 | Same biological sex observers are now required for directly observed urine collections under DOT rules. |

| Insurance testing uses a broader panel | Insurers screen for substances beyond the SAMHSA five, including nicotine and benzodiazepines, for risk assessment purposes. |

| A clean DOT test does not equal insurance approval | Federal and insurance panels differ in substances, cutoffs, and look-back periods; passing one does not guarantee the other. |

| Prescription disclosure matters in underwriting | Documented, consistent prescription use is rarely penalized; undisclosed use leads to denial or higher premiums. |

What I’ve learned from watching employers get this wrong

The most common mistake I see is employers treating drug testing as a single compliance checkbox. They update their DOT policy, confirm their collection site is certified, and consider the job done. Then an employee applies for a life insurance policy through a group benefit program, tests positive for a benzodiazepine they never disclosed, and the employer’s HR team has no idea how to respond because they never built a process for that scenario.

The federal and insurance frameworks are genuinely separate systems. They were built by different agencies for different purposes, and they measure different things. A DOT-compliant urine collection with a five-panel SAMHSA screen tells you nothing about whether that same person would pass an insurance paramedical exam. Underwriters look at nicotine, alcohol metabolites, and prescription drug patterns that never appear in a federal workplace test.

The oral fluid situation is another area where I see confusion. Employers read that oral fluid testing was authorized in 2023 and assume they can use it now. They cannot. No certified labs exist yet. Until two HHS-certified oral fluid labs are operational and the Federal Register announces the transition window, directly observed urine collection is the only compliant option when oral fluid is required under a program. Employers who skip the observed collection because they think oral fluid is available are creating real regulatory exposure.

My advice: build two separate compliance tracks. One for federal workplace testing, one for insurance-related screening. Give each track its own policy document, its own DER contact chain, and its own training module for HR staff. The overlap between the two is smaller than most people assume.

— Alan

Countrywidetesting’s drug testing services for 2026 compliance

Employers managing both federal and insurance-related drug testing obligations need a testing partner whose labs meet the standards both systems require.

Countrywidetesting provides lab testing services certified to meet DOT and SAMHSA standards, covering the full five-panel federal requirement and expanded panels suited for insurance screening assessments. Every sample is processed through licensed laboratories holding SAMHSA, ISO, CLIA, and CAP certifications. For employers who need flexible options, Countrywidetesting also offers at-home drug test kits covering 12 substance categories, giving HR teams a practical tool for pre-employment and insurance-related screening outside a clinical setting.

FAQ

What substances does federal workplace drug testing cover in 2026?

SAMHSA requires testing for five categories: amphetamines, cocaine, marijuana, opiates/opioids, and PCP. Specimen validity testing is also required to confirm sample integrity.

Can employers use oral fluid testing for DOT compliance in 2026?

No. No HHS-certified oral fluid laboratories are operational as of mid-2026, so employers must use directly observed urine collections until two labs are certified and the Federal Register announces the transition window.

Does passing a DOT drug test guarantee life insurance approval?

Passing a DOT test does not guarantee insurance approval. Insurance underwriters use broader panels with different cutoff thresholds and look-back periods, so the two processes produce independent results.

How do insurers treat disclosed prescription medications in drug testing?

Insurers evaluate disclosed prescriptions against the applicant’s medical records. Consistent, documented prescription use is rarely penalized, while undisclosed use typically leads to denial or higher premiums.

What happens if an employee refuses a directly observed urine collection?

Under DOT rules, refusing a directly observed collection is treated as a positive test result, triggering disciplinary action and regulatory reporting requirements for the employer.